[#11] What's next🤔? 2021 Predictions

[#11] What's next🤔? 2021 Predictions

Here's our best guess at what lies in store for the world of Biz-Tech in 2021

Author’s Note

Happy New Year dear readers and hope you had a wonderful holiday. Readers really liked our last week’s piece on Slack x Salesforce and that also helped us find some audience in the Venture Capital space in India and the US.

For the new readers

This space is where we (Aditya and I) write essays on topics that we’re trying to understand. In a typical week, I juggle between Solutions Architecture, Product Management and Angel Investing. However, everytime I open this column, I try to become an independent analyst. Mostly, that means I try to work out what questions to ask.

The Inspiration & The Genesis

2020 should have been the year that ended year-end prediction pieces, one would hope. After all, a global public health crisis, unlike any other that we have faced, was virtually missing from every 2020 forecast/prediction report published in December 2019.

Still, since Christmas, several reporters/analysts have been chronicling how the future could look like in 2021. Maybe they were looking to find a reason to believe or a reason not to work too hard during the holiday break. However, one must also realize that a prediction's value is not accuracy but the reasoning that follows and acts as a catalyst for thought. It also takes an awful amount of courage to predict something in public, but it does lubricate our reasoning's rails if done rigorously.

So in that spirit, here’s a non-exhaustive list of macro-trends, loosely grouped into themes I’m particularly excited about. Sharing them is a way to connect more dots, meet and talk to more founders, and solicit inputs to develop these ideas further. I’d love to hear your thoughts, too, in the comments.

Creative talent would want to own their audience directly

Thanks to the internet, a breakout star no longer needs to sign a contract with a TV-network or a radio-station. Ad-supported and algorithmically driven platforms like YouTube, TikTok, Instagram, and Spotify ensure that creative talents get in front of the right audience. However, providing a similar reach to every new creator keeps becoming difficult for the platform as they scale.

As creators begin to realize the platforms' limitations, they’d want to own their own audience. We could well see an emergence of SaaS toolkits that bundle all the things necessary to power a business associated with an individual’s brand. Equivalents of Substack (mailing & podcasts’ subscribers’ list) will emerge in the video, audio, community-products and other ways to build, manage and monetize your audience. Tools like Buy Me a Coffee, Patreon, PubNinja, and OnlyFans are early breakouts and give us a sense of what is possible. We’re talking about Cardi B making $8M per month on OnlyFans kind of potential.

If you’re a talented content creator of any kind, you would soon be able to spin up a community to build and gather your audience and layer it with other adjacent services to manage, engage and monetize your audience on a Shopify-esque platform. This could well reduce social platforms like Instagram, YouTube, and TikTok to being top-of-funnel marketing initiatives where the goal is to direct everyone you reach on the platform to your own privately owned & managed channel.

With the emergence of powerful & integrated tools to create and distribute content effectively, every company will soon become a content company that will subsequently turn talented content creators into brands who own the relationships with their own audiences. Expect to see a massive acceleration of this trend in the year(s) ahead.

Enterprise Cloud Software will consolidate

When we talk about enterprise and cloud computing, consolidation is the obvious trend for the coming year. As we noted in our previous piece, Salesforce’s acquisition of Slack was among the biggest stories of the year. Simultaneously, Salesforce is just one of the several massive enterprise software companies with deep pockets and an insatiable growth appetite. A name that immediately comes to my mind is Zoom - by all accounts, Zoom had a terrific year, but its stock price is likely inflated.

Many well-known but barely profitable enterprise software companies could be the next Slack or Segment (acquired by Twilio). Dropbox, New Relic, Box, SurveyMonkey, Smartsheet, and Domo all have single-digit billion market caps with established customer bases and high NPS products. All of these would make ideal acquisition targets for companies with enterprise distribution that want a consumer-grade product DNA to create a perfect bundle and fend off competition.

Many cloud companies with inflated market caps will go on an aggressive acquisition spree to acquihire companies with a lot of revenue potential. Reports suggest that Zoom might be building an email and a calendar service to next - however, a better approach may be to acquire someone like a Calendly. Better still, if the motive is to take on the bundles of Microsoft/Google, a gangster move could be to acquire a workflow collaboration company like Notion/Coda and/or Dropbox (Dropbox Paper) and/or Rocket Chat.

Changing definitions of the cloud will trigger different customer expectations that'd push major cloud vendors (IaaS & PaaS) to differentiate. And the easiest way to do that? Follow the Microsoft playbook - acquire an open-source tool and create proprietary integrations while still allowing others to keep using it as an open-source tool. In case you didn't pick it up, I'm talking about Github. With the community/interface products having been acquired (Slack & Github), I predict that the next theme of acquisitions to be around data - analysis, management, databases et al.

Following the theme and framework outlined above, Databricks, Redis, and Kong could be acquisition targets for companies like ServiceNow and Snowflake. MongoDB could be a good target for companies like Microsoft and Oracle. SmartSheet, the project-management collaboration tool, could also be a top contender.

A logical deep dive into the specifics deserves a separate piece and we’d do that later.

Creativity & Collaboration would be the new theme for enterprise tools

Being more productive was the best way to stand out at work until the dawn of software. As software and algorithms supplant mundane and repetitive tasks at the workplace, expect many of them to be automated/obsolete. The benefit of that would be human labor, shifting into new skills and capabilities. Most important of them: creativity. Impressive graphics that spit life into dull presentations, creative ways to visualize data (using natural language being one), better ways to communicate effectively (asynchronous video communication tool), ability to create powerful prototypes and mockups that’d have been a result of several dozens of meetings. We expect most of these capabilities to be embedded into every workplace as these capabilities will drive outperformance at work, school, social platforms, everywhere.

As Scott Belsky puts it, the massive broadening of the market is aimed to serve two different sets of user personas -

The Content-First Creator tools: they start with a video, image, or graphic and then deconstruct or remix

The Collaboration-First Creator tools: they start by bringing together a group of people with varied skillsets and leveraging their shared assets

Of course, we’ll see a lot more tools emerge out on new platforms like the web and mobile, but their success will depend on two critical factors - finding & solving for whitespace and the ability to build moats through certifications -

Finding & Solving for whitespace: The rise of low/no-code tools would enable everyone in an organization to be a creator. Think building custom CRMs using Notion, low-code collaborative apps to customize your workflows using Airtable, easy-to-create powerful designs using Figma and/or creating marketing material/illustrations using Loom. But how to find the whitespace is the key question, and it’s actually not that hard. Two or more product teams at a huge corporation find it very difficult to collaborate and create a seamless experience for their (mutual) end-users. They typically prioritize breadth of usage over breadth. Calendly exists because Gmail & Calendar teams at Google haven’t worked together to create a seamless experience for that use case. Similarly, Loom might succeed because Gmail, Video, and Meet teams are probably too busy to care about that opportunity. Similarly, Dropbox Paper isn’t difficult to replicate for Google. Understanding these nuances would help to find the next whitespace worth solving for.

Ability to build moats through certifications: Enterprises tools have different procurement cycles that are long and typically driven by long-term relationships with your sales teams. Few players have the scale, capital, distribution, and network effects as moats. Most niche players need to differentiate on the product-side and create a moat, like differentiated-technology competitors cannot easily replicate. However, the new upstarts would have to create learning academies, and certification programs - Cisco, Salesforce, Oracle, Microsoft have nailed this one. Once people learn the technology, you give them credit through certifications. And once they do, they don’t want to move off those products. The more popular a technology is among enterprises, the more people want to learn it. The skilled talent is an added incentive for an enterprise to incorporate that tool into their tech stack. Stitch all of it together into one platform, and you get the perfect recipe for a viral flywheel.

To sum it up: creativity would be the next new theme for enterprise tools just like productivity was for the tools of the last decade. Collaboration-first would be the central theme for these tools and each of them could have an end-to-end stack starting with mastering the tool, obtaining a certification to put it as a skillset and a portal to find jobs where these skills are in demand. No tool owns the space currently and I expect a lot of product innovation to follow as we have ~$210B in revenues at stake, possibly recurring in nature.

Fintech, entertainment & commerce will be embedded everywhere

Fintech

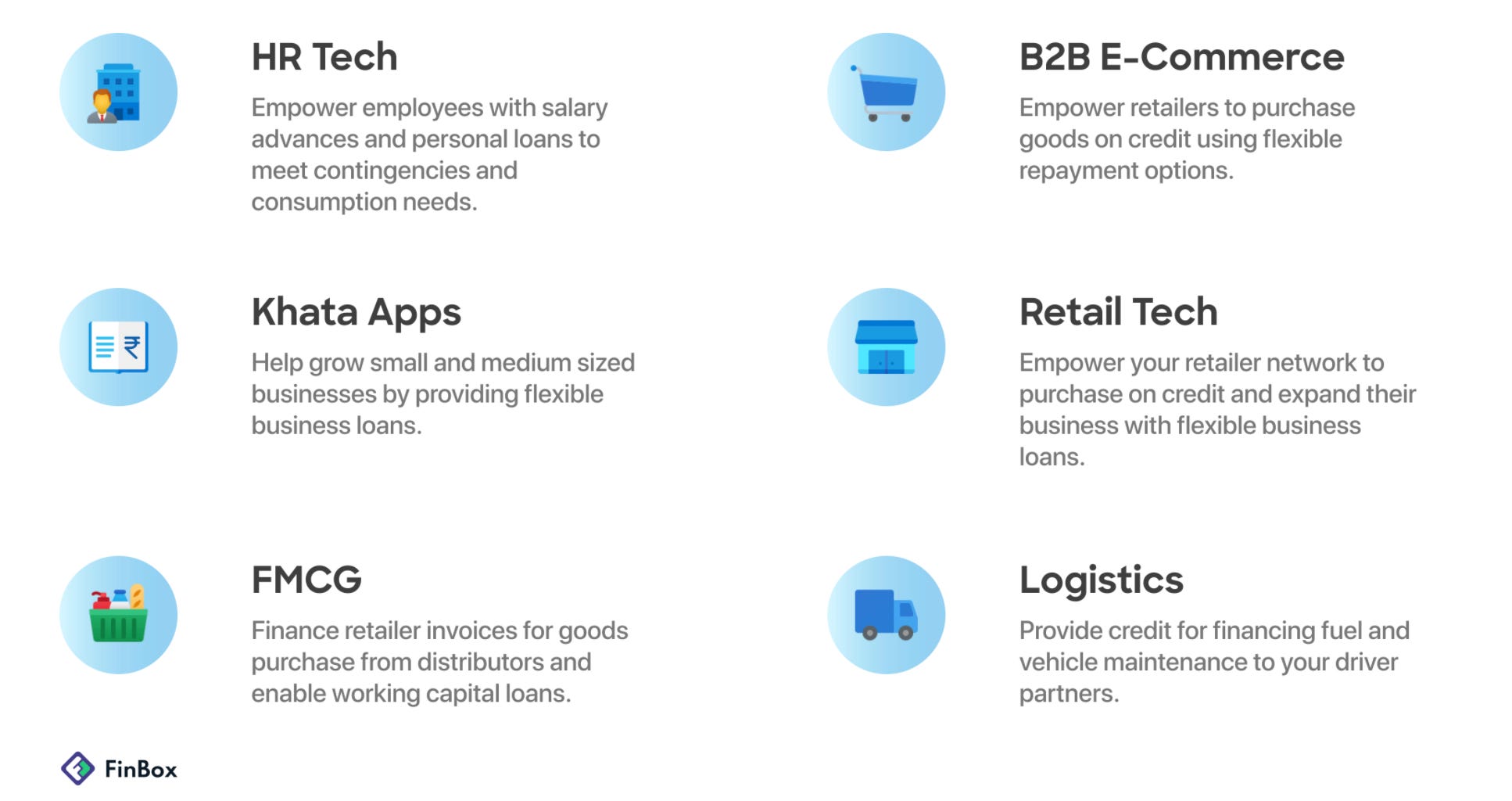

As a McKinsey study puts it, the economic profit of the world’s top banks and insurance companies declined by $800B and $300B respectively between 2015 and 2018, making them among the two worst-performing sectors globally. The COVID crisis only made these trends worse. That leaking value, though, is up for grabs with a host of startups competing for that wallet-share. This is now being called embedded finance - it’s best understood by integrating a financial service/product into a non-traditional financial product (think Whatsapp offering payments as a feature). Embedded finance is popping up everywhere and is projected to be worth $7 Trillions by 2030 and will allow all companies to drive a significant portion of their revenues from financial services. A few examples follow -

This isn’t certainly a new trend but the explosion of consumer internet products for our everday lives and the ease with which we can integrate them across verticals and businesses using APIs and data commons. Couple that with the low NPS scores for traditional financial institutions and the existing inefficiencies in their processes, we get a massive tailwind to ride.

Entertainment & Commerce

In 2020, American adults were expected to spend 20 more minutes on their mobile devices than on TV. Out of the 3:49 spent on mobile devices, over 3 hours were spent on apps, and yet, people aren’t downloading any more apps. Couple that with an average American downloading 0 apps every month. It’s all about using the same apps for longer durations.

From consuming entertainment pieces on the internet to buying things online from SMEs, things that were once siloed to particular fringe players residing on the web's long-tail aren’t migrating over to mobile phones. But since a good chunk of the internet's GDP is through these apps, I expect them to move into apps with an established userbase. As a consequence, you get super apps. Those of you who are aware of my virtual investment portfolio know my obsession with this macrotrend.

Simply put, super apps pick an existing product and offer it as a feature inside their own for their existing userbase. Facebook did that with press/media, WhatsApp is doing that with payments & Headspace launched a 3-part meditation module inside Netflix recently. Super apps are no longer buzz words. It’s a real secular trend in the way technology products will be built shortly. It’s also a highly complex trend to evaluate, both as an investor and a consumer. But the following are some lenses you can use to understand this trend better, a micro-thesis if you will -

High-frequency transactional apps in China & SEA use low-margin businesses like food-delivery or micro-payments and attacking low-frequency, high-margin businesses at low to zero customer acquisition costs. They’re leveraging their distribution and their understanding of the end-user and thinking of what other revenue streams that they can create with that mindshare. Meituan in China & Paytm in India started with food delivery & micro-payments initially but account for a major share of OTA bookings in their respective countries.

Low-frequency transactional apps have a very different approach to super apps. The overarching objective is to gain that customer mindshare and do that by bypassing SEO/PPC costs. At the Flipkart scale, the marginal costs of distributing video and/or games are minimal, as Hitanshu Gandhi puts it here. It’s a clever hack to establish customer mindshare by escaping search/social media and making fewer people uninstall the Flipkart app when not in use, as we explored here. I see a lot more niche content and SDK-powered Real Money Games & E-Sports coming inside apps like Flipkart, Paytm & CRED soon. Also, expect this trend from the east come to the west.

Subscription businesses tend to benefit very differently from a super-app/embedded entertainment strategy. At scale, subscription businesses need to balance the breadth and depth of usage by their users. The easiest way to do it is usually to club something that is loved (high NPS) but low margins with your existing subscription/bundle for one or more of the following -

Reduce churn

Increase renewals

Increase conversions

Netflix and Headspace launching modules for meditation is a similar move.

Another sub-trend is that everything is going to become commerce and transaction-related. We spend a lot of time in social apps, video apps, and communication apps. They already have a lot of our mindshare and know a lot about us. Couple this with their plateauing ARPU (Average Revenue Per User) growth, and you’d get perfect distribution vehicles for commercials we all want to watch with aligned incentives for both sides. Consumers get the convenience of getting an integrated offering within the same set of apps they’re power users of. The apps can now turn their existing ad-units into transactions and increase the revenue-making from the pixel area. I’d already written about this way back here and here.

Entertainment modules like gaming (RMG + E-Sports), podcasts and videos will be featurized and embedded everywhere - not always with the intention to make more revenue but sometimes to reduce customer churn or avoid the search/social media tax as this is the easiest way to provide a differentiated offering.

As we spend more time on the platforms, expect ad-supported ones to make their ads transactional in a bid to increase their revenues from that particular unit on our screens. I anticipate the day isn’t far when we might buy financial products/insurance on YouTube using Google Pay

This is turning out to be a very long read. Let’s take a small break and if you’re reading this newsletter for the first time, please take a moment and consider subscribing to it -

New tools for the future of work

When we’d looked ahead to the new year in 2019, we had no idea of the magnitude of changes we’d confront in 2020. Employees were fired, freelancing based on micro-skilling was the new normal. Among other things, for many businesses, the pivot to a fully-remote workforce seemingly happened overnight. It forced employers to adapt on the fly when rethinking how their employees get work done. Rapid innovations to bridge the gap and keep the workforce moving forward was the theme for the initial few months. Still, as everyone realizes that this will be the new normal in the short-medium term future, there’s an opportunity to build tools for the future of work in 2021. For an easier understanding, let’s break this down to the 2 user-cases the tools would attempt to solve for -

Cybersecurity: Security can no longer be optimized for use in-office only. The flexibility in location allowed by remote work is here to stay, at least in some capacity, for most companies. However, this is bound to give sleepless nights to your IT Admins, and if you work at a large MNCs, you’d probably understand why. Corporate networks and resources have to remain impregnable, and the security measures for accessing them must be robust, offering similar levels of protection as being in the office. As more companies pivot to allowing employees to work remotely, it’ll now be incumbent on the IT teams to build/provide applications and system architectures paramount to allow for a safe, authenticated access, agnostic to the location the employee is logging in from. This is a massive opportunity for cybersecurity startups. Companies like Yubico are leading the revolution. They did $41M in revenues in 2019 and $100M in 2020 and I’d expect at least a 50%+ jump given the WFH trend.

Content Creation tools for Prosumers: Among other things, 2020 accelerated video consumption and made e-commerce the new normal. Superimpose these two trends, and you get a whopping $137B a year industry in China. To put some context on how large this number is, the US's digital ad industry is ~$140B a year. As sellers start leveraging video over photos to sell products and where buyers browse through video catalogs looking for entertainment, expect the live stream e-commerce industry to be akin to professional content production. It’d be professional-grade programming with scripted selling sessions hosted by sellers/influencers who are no less qualified than TV actors, all done in high-end lighting with the help of professional make-up artists, rented wardrobes & sets, production managers & sound editors. With video destined to become high-fidelity productions, I expect a lot of product innovation to happen across the value-stack as it’s part entertainment, part supply chain, and part game show. And a big part of this would be software-enabled, across devices, collaborative, and easy on the browser. A host of tools like Mux, Descript, and InVideo have just scratched the surface but have set the stage for others to follow.

With remote work extending well into 2021 for many businesses and even becoming semi-permanent for others, we see an opportunity for new applications, tools and architectures to emerge that support both synchronous and asynchronous means of connection and collaboration that allow for a safe, authenticated and secure access to their databases.

Thanks to COVID, retailers are forced to pursue new ways to sell to customers beyond the physical stores, shoppers have a lot more free time to try out new apps and influencers are looking for new ways to engage and monetize their audiences.

Corporate Venture Capital goes mainstream

2020 saw a few mega IPOs, and the first few months’ performances were a major win for the companies and investors who backed them early. Among those who scored big were a few public companies like Salesforce, whose $400M investment in Snowflake is now worth $1.6B. Snowflake investment was not one-off but rather something that cemented the trend of Salesforce’s string of hugely profitable deals in up-and-coming startups. Some of its significant deals over the past decade include - MongoDB, Twilio, Box, DocuSign, Snowflake, and Zoom. Often Salesforce’s investment gains often exceed the income from its core business. For the most recent quarter, Salesforce reported a $1.04B profits in investments while the core business's operating income was $224M.

Salesforce isn’t the only valley-based company to do that. Stripe has invested in over 15 startups so far, most of those investments coming in the fintech space, adjacent to the ones Stripe works in. Similarly, Slack invests in many startups (Loom being one of the popular ones) that it thinks its users will love when integrated with Slack’s metaverse. More recently, in 2018, the cryptocurrency trading company Coinbase launched Coinbase Ventures to establish a financial system built on digital currency.

Corporate Venture Capital is usually set up to encourage a niche's development as a layer on top of its ecosystem, further strengthening it. Put another way; it allows companies to own a stake in future innovation that could benefit them without allocating significant human capital. 2021 could be the year it goes mainstream for the following reasons -

Mega IPOs like Doordash, Snowflake, Airbnb, and some companies like Zoom will probably realize they’re overvalued at the moment and would want to invest the capital that lends them a strategic edge before the markets correct themselves. Zoom already is exploring office communications space (email + chat + office telephony) but a lot of this is a hardware component that has long sales cycles. So maybe it can consider entering into post-sales communications market? Cloud-based Contact Center-as-a-Service? On the other hand, Snowflake would likely want to own a system of engagement in the enterprise SaaS space as larger cloud vendors double down their efforts in the space. I'd not be surprised if they buy a startup in the data observability space.

This will likely be also catalyzed by the realization of a few ventures that building an ecosystem is hard. Following on the playbook of a Slack or even Zerodha, I expect Jio Platforms, CRED, and Flipkart to go on an acquisition spree. For example, some ideas for CRED could be to act as a launchpad for D2C brands, as an incubator almost to allow them to flourish taking in equity or even doing vendor-financing/revenue-based financing. Or even set up an investment arm to invest in new-age fintech products aimed at CRED’s users. CRED provides the distribution while their investments provide an added incentive for the upstarts.

Corporate Venture Capital could either be a strategic investment or be a purely financial one but it’d go mainstream in 2021, especially in India. Zerodha could fund the next ET Money while CRED could fund the next Small Case. Slack and Stripe would keep investing in newer upstarts who help deepen their ecosystem for their customers by pushing the switching costs higher.

Well, that’s about it. Wow! That turned out to be a very long piece and if you’re with us still, thank you. We hope this helps you get as excited about 2021 and this decade as us.

Do take a look at our previous posts here. If you find this interesting, please consider sharing it forward -

As always, we look forward to your thoughts, comments, and feedback.

How did we do this week? Please click on a link to vote 👇🏼-

Sincerely,

👇🏼 please hit the ♥️ button below if you enjoyed this post.